Chapter 7 Bankruptcy Cost: What Homeowners Should Expect Before Filing

Debt has a way of creeping up quietly until one month, it stops feeling manageable and starts feeling impossible. If you're a Nebraska homeowner researching Chapter 7 bankruptcy, you're likely doing so in the middle of a genuinely hard season of life. Maybe you're behind on mortgage payments, buried in medical bills, or facing a wage garnishment that's draining your paycheck before it even lands.

Whatever brought you here, the most important thing you need right now is honest, clear information, not a sales pitch and not a legal lecture.

This guide breaks down the real cost of Chapter 7 bankruptcy and what homeowners should expect. How much does Chapter 7 bankruptcy cost, really? We'll walk through every line-item expense, explain what the process means specifically for homeowners with equity in their property, and lay out a side-by-side comparison between the bankruptcy path and another option many Nebraska homeowners never consider: selling their home for cash to eliminate the debt.

What Is Chapter 7 Bankruptcy?

Chapter 7 bankruptcy is a federal legal process governed by the U.S. Bankruptcy Code. It allows qualifying individuals to permanently eliminate most types of unsecured debt, including credit card balances, medical bills, personal loans, and unpaid utility accounts.

The process works like this: a court-appointed bankruptcy trustee reviews your financial situation, liquidates any assets that aren't protected by state exemption laws, and uses the proceeds to repay creditors partially. Any remaining eligible debt is then legally discharged. In exchange, your financial slate is wiped clean.

The moment your Chapter 7 petition is filed, a powerful legal protection called the automatic stay goes into effect. This court order immediately stops all creditor collection activity, no more calls, no lawsuits, no wage garnishments, and no foreclosure proceedings for the duration of your case. For many filers, that immediate relief is worth as much as the eventual debt discharge.

A standard Nebraska Chapter 7 case runs approximately 90 to 120 days from filing to final discharge, making it significantly faster than Chapter 13, which can stretch across three to five years.

How Chapter 7 Differs From Chapter 13

Understanding the difference between the two primary personal bankruptcy options is essential before you can evaluate the true chapter 7 bankruptcy cost and decide if it's the right path.

Who Chapter 7 Is Designed For

Chapter 7 is specifically built for individuals who have limited income, significant unsecured debt, and few non-exempt assets. It's the fastest and, in many cases, the most effective form of consumer debt relief available. Research from one Nebraska-based bankruptcy firm reviewing 172 cases found a 98% discharge success rate for Chapter 7, a figure no other debt relief option comes close to matching.

That said, Chapter 7 is not universally the best choice, especially for homeowners who have built up meaningful equity. Understanding what happens to your home during the process is critical, and we'll cover that in detail later in this guide.

How Much Does Chapter 7 Bankruptcy Cost? The Full Breakdown

When people search for chapter 7 bankruptcy cost: the real, all-in number, not the advertised figure that conveniently leaves out mandatory fees.

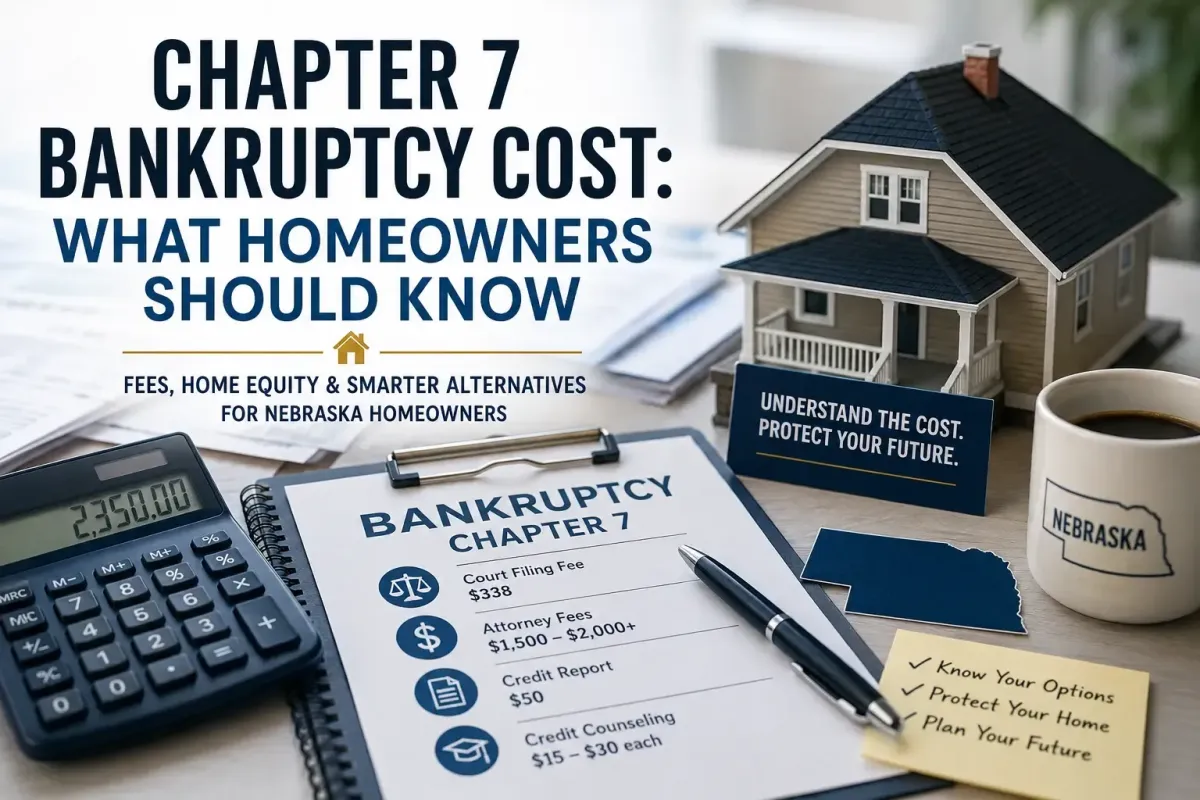

For a straightforward consumer case in Nebraska, the total cost to file Chapter 7 bankruptcy typically falls between $1,900 and $2,400. Some simple, well-organized cases come in closer to $1,800. More complex cases, particularly those involving real estate, multiple creditors, or disputed exemptions, can reach $2,500 to $3,500 or more.

That total breaks down across four distinct categories, each of which you should understand independently.

Many attorneys advertise only their legal fee, not the mandatory court filing fee, credit report, or required courses. When comparing quotes from bankruptcy attorneys, always ask for an all-in total to make a true apples-to-apples comparison. A quote of "$1,500 attorney fees" can easily become $2,100 once all required costs are added.

The Chapter 7 Court Filing Fee

The Chapter 7 court filing fee is a federal government charge paid directly to the U.S. Bankruptcy Court. It is non-negotiable, the same at every court nationwide, and must typically be paid in full before your case is opened.

As of 2025, the Chapter 7 filing fee in Nebraska is $338, structured as follows:

In rare and documented cases of extreme hardship, a filer may petition the court to pay this fee in installments up to four payments spread over 120 days. A full fee waiver is available only in truly exceptional circumstances where the applicant's income falls below 150% of the federal poverty line. For most filers, the $338 is simply part of the upfront cost.

Attorney Fees for Chapter 7 Bankruptcy

Chapter 7 lawyer fees represent the largest single expense in almost every case. In Nebraska, you can expect attorney fees to fall within the following ranges based on case complexity:

Well-organized, simple case: $1,400–$1,700

Typical consumer case: $1,700–$2,000

Moderately complex (assets, multiple creditors, real estate): $2,000–$2,500+

Several factors directly influence how much you'll pay in Chapter 7 lawyer fees:

Case complexity. Multiple creditors, business-related debts, real estate equity questions, or pending lawsuits all require more attorney time and push fees higher.

Your level of preparation. Attorneys bill for the time it takes to gather your information. Clients who arrive with 6 months of pay stubs, 2 years of tax returns, and a complete creditor list save hours of administrative work and pay meaningfully less as a result.

Honesty and transparency. Experienced bankruptcy attorneys and federal trustees are highly skilled at identifying financial inconsistencies. When clients are less than fully transparent, attorneys spend additional billable time piecing together the picture. Laying everything out from the first consultation keeps both your case and your costs cleaner.

Attorney experience. Counterintuitively, the most experienced Nebraska bankruptcy attorneys often charge rates similar to those of less experienced practitioners. The difference is that a seasoned attorney gets the case done right the first time, avoiding costly mistakes, dismissals, or re-filings.

Watch Out For Split-Fee Schemes: Some attorneys advertise Chapter 7 for as little as $75–$300 upfront by dividing their fee into "pre-filing" and "post-filing" work. The U.S. Trustee Program has consistently flagged this practice as problematic. What looks like a bargain upfront often results in a total bill of $2,400 or more, and sometimes leads to ethical complaints against the attorney. If a quote sounds too good to be true, it almost certainly is.

Required Credit Counseling Courses

Federal bankruptcy law mandates that every filer complete two separate courses, one before filing and one after:

Pre-bankruptcy credit counseling: Must be completed within 180 days before filing your petition. A completion certificate is required as part of your filing documents. Cost: approximately $15–$30, paid directly to a court-approved provider.

Post-filing debtor education: Must be completed after your case is filed but before your discharge is granted. This course covers budgeting and personal financial management. Cost: approximately $15–$30, again paid directly to the provider.

These courses are completed online or by phone and typically take two to three hours each. Your attorney will recommend approved vendors, but you handle registration and payment directly. Some providers offer fee waivers for qualifying low-income filers.

Additional Costs You May Not Expect

Beyond the three primary expense categories, several smaller but real costs can add to your total:

Average Cost of Chapter 7 Bankruptcy in Nebraska

Now that we've broken down each component, here's how the average cost of Chapter 7 bankruptcy stacks up for Nebraska filers across different case types.

Total Cost of Chapter 7 Bankruptcy: Simple vs. Complex Cases

For Nebraska homeowners specifically, cases almost always land in the "average" or "moderately complex" bucket because the moment your home is part of the picture, the trustee's review becomes more thorough, and your attorney's preparation time increases accordingly.

The critical question of what happens to your home is where the true cost of Chapter 7 for property owners gets fully revealed.

What Happens to Your Home in Chapter 7 Bankruptcy?

This is the question that matters most to homeowners, and it's one that many online guides gloss over. It depends on how much equity you have and whether that equity exceeds Nebraska's homestead exemption.

Nebraska Homestead Exemption Explained

Nebraska law protects a portion of your home equity from the bankruptcy trustee through what is known as the homestead exemption. Under Nebraska Revised Statute § 40-101, this exemption protects up to $60,000 in home equity for individual filers. In cases where the property is jointly owned by a married couple, the combined exemption may provide greater protection depending on how the deed is structured.

Here's what this means in practical terms:

If your home is worth $220,000 and you owe $190,000 on your mortgage, your equity is $30,000, fully protected by the exemption. The trustee cannot force a sale.

If your home is worth $250,000 and you owe $160,000, your equity is $90,000 $30,000

Nebraska bankruptcy trustees are paid a commission on non-exempt property they successfully liquidate. If there is real equity above the exemption threshold, trustees have both the authority and the financial incentive to pursue it.

What If You Have More Equity Than the Exemption Covers?

If your home equity exceeds the Nebraska homestead exemption, the Chapter 7 trustee has several options:

Sell the home, pay off the mortgage, return your $60,000 exempted amount, and distribute the remainder to creditors.

Negotiate a buyout. Your attorney may arrange for you to pay the trustee the non-exempt equity amount in cash in exchange for keeping the home.

Abandon the property if the excess equity is marginal or the cost of sale outweighs the benefit to creditors.

Option 3 happens more than people expect, but it is entirely at the trustee's discretion, not yours. If you have significant equity, you cannot count on the trustee walking away from it.

Real-World Example: A Nebraska homeowner owes $40,000 in credit card debt and has $85,000 in home equity. They filed Chapter 7, hoping to eliminate the credit card debt. Under Nebraska's $60,000 homestead exemption, $25,000 of their equity is exposed. The trustee has the legal authority to sell the home, return $60,000 to the homeowner, and use the remaining $25,000 (minus sale costs) for creditors. The homeowner eliminates $40,000 in credit card debt but loses their home in the process. This is the outcome that many homeowners don't anticipate when they file.

Reaffirmation Agreements and Your Mortgage

If you're current on your mortgage and your equity falls within the exemption limits, you can typically keep your home by signing a reaffirmation agreement, a written contract between you and your lender confirming you'll continue making payments despite the bankruptcy. This agreement is voluntary and removes the mortgage from the discharge, meaning you remain personally liable for the debt.

Reaffirmation is the standard path for homeowners who want to keep their property in Chapter 7. However, if you are significantly behind on mortgage payments, your lender may refuse to enter a reaffirmation agreement, leaving the future of your home uncertain.

Chapter 7 Bankruptcy vs. Selling Your House for Cash: A True Cost Comparison

For many Nebraska homeowners, the goal isn't bankruptcy itself, it's debt relief and financial freedom. Chapter 7 is one path to that goal. Selling your home to a direct cash buyer is another option, and depending on your situation, it may be faster, cheaper, and far less disruptive to your financial future.

For a homeowner with $60,000–$100,000+ in equity, a cash sale can generate enough proceeds to pay off credit cards, medical bills, tax liens, and back mortgage payments, eliminating the need for bankruptcy. And because the home sale doesn't affect your credit, you're free to rent or eventually purchase again without a bankruptcy on your record.

Nebraska homeowners across Omaha, Lincoln, and dozens of other communities have used exactly this approach to escape financial distress without the long-term consequences of a bankruptcy filing.

How to Qualify for Chapter 7 Bankruptcy in Nebraska

Not every homeowner qualifies for Chapter 7. Federal law requires passing the Nebraska Means Test, a two-part calculation that determines whether your income is low enough (or your expenses high enough) to justify Chapter 7 relief rather than a structured repayment plan.

The Nebraska Means Test Explained

Step 1: Compare your income to Nebraska's median. Calculate your average monthly gross income over the past six calendar months and annualize it. If your figure is below Nebraska's current median income for your household size, you automatically qualify for Chapter 7. No further calculation needed.

Step 2: If your income exceeds the median, you move to the full Means Test calculation. This involves subtracting IRS-standardized living expenses, secured debt payments (mortgage, car loan), priority debt payments (taxes, child support), and other allowable deductions from your income. If the result of your "current monthly disposable income" is low enough, you may still qualify for Chapter 7.

One of the most valuable things a skilled Nebraska bankruptcy attorney does is present your income and expense picture in a way that accurately demonstrates Chapter 7 eligibility. The calculation is technical, and the margin between qualifying and not qualifying can be surprisingly narrow.

Nebraska Median Income Limits (2025–2026)

Note: These figures are updated every six months by the U.S. Trustee Program. Verify current thresholds at justice.gov/ust before filing.

If your household income falls below these thresholds, Chapter 7 is very likely an accessible option. If you're above the median, consult an attorney before assuming you don't qualify. The Means Test's expense deductions often bring otherwise ineligible filers into the qualifying range.

5 Practical Ways to Reduce Your Chapter 7 Bankruptcy Costs

If you've weighed your options and determined that Chapter 7 is the right path, there are concrete steps you can take to keep the cost of filing Chapter 7 bankruptcy as manageable as possible.

1. Arrive at your consultation fully prepared. Bring at least six months of pay stubs, two years of tax returns, six months of bank statements, a complete list of every creditor with their approximate balances, and a copy of your government-issued ID and Social Security card. Attorneys bill for the time it takes to track down missing documents. An organized client genuinely and measurably reduces attorney hours, which reduces your bill.

2. Be completely honest with your attorney from the first conversation. Federal bankruptcy trustees are experienced professionals with access to financial records, property databases, and years of pattern recognition. Attempting to hide assets, underreport income, or obscure recent property transfers doesn't work and creates significant legal risk while adding billable time as your attorney pieces together an incomplete picture. Full transparency from the start is both the ethical and the financially smart approach.

3. File at the right time, not later. The Means Test is based on your income over the prior six calendar months. If your income has recently dropped due to job loss, medical leave, reduced hours, or divorce, filing promptly locks in that lower figure and may make the difference between qualifying for Chapter 7 and being pushed toward Chapter 13. Waiting has real financial consequences when eligibility hangs on a six-month income window.

4. Complete your credit counseling courses promptly and independently. These required courses are handled directly by you, not your attorney. Taking them quickly keeps your case moving, prevents delays, and ensures your attorney doesn't need to follow up on missing completion certificates (which adds billable time). Most online courses take two to three hours and cost $15–$30.

5. Get itemized quotes from at least two or three attorneys. The Nebraska bankruptcy attorney market is competitive, and fees do vary. That said, don't make the cheapest quote your primary criterion; a poorly prepared filing or a dismissed case costs far more than the few hundred dollars saved on a lower-priced attorney. Look for transparency, a clear all-in fee quote, Nebraska-specific experience, and a genuine willingness to answer your questions before you commit.

Is Selling Your Home an Alternative to Bankruptcy?

For Nebraska homeowners, this question is worth asking with real seriousness because the answer, in many situations, is yes.

When Selling Your Home Makes More Financial Sense Than Filing

Consider a cash home sale rather than Chapter 7 if one or more of the following apply to your situation:

Your home has significant equity above the Nebraska exemption. In Chapter 7, the equity is exposed to the trustee. In a cash sale, that equity becomes your money available immediately to pay off the debts that are driving your financial crisis.

Your primary debts are secured, not unsecured. Chapter 7 discharges credit cards and medical bills, but it does not eliminate your mortgage. If your biggest financial burden is your housing payment, selling the home addresses the root cause in a way bankruptcy cannot.

You are behind on mortgage payments and facing foreclosure. Once foreclosure is initiated, a cash sale may be the only option that preserves any equity and avoids a court-forced sale at a depressed price. A cash buyer like Launch Homebuyers can close in days, stopping the foreclosure process and putting money in your hands.

Protecting your credit matters for your near-term plans. If you intend to rent an apartment, apply for a job with a credit check, or purchase another property within the next several years, a Chapter 7 bankruptcy staying on your record for 10 years is a serious obstacle. A home sale carries no credit consequences.

You want this resolved in days, not months. The bankruptcy process, even at its fastest, takes three to four months of filings, waiting periods, and a federal court appearance. A cash sale can be completed in as little as seven days.

How a Cash Sale Through Launch Homebuyers Works

At Launch Homebuyers, we've helped Nebraska homeowners in exactly these situations, behind on payments, overwhelmed by debt, unsure of their options, find a clean, fast exit without the cost or consequences of bankruptcy.

Our process is straightforward:

Tell us about your property. Fill out our short form or give us a call. No commitment, no obligation.

Receive a fair cash offer within 24 hours. We assess your home's condition and market value and make a real offer, no games, no lowballing, no pressure.

Close on your timeline. We can close in as few as 7 days, or on whatever date works best for your situation.

We pay 100% of closing costs, charge zero commissions or fees, and purchase homes in any condition, no repairs, no cleaning, no staging required. The cash you receive at closing can be directed to pay off exactly the debts that are causing your financial distress.

We've completed 500+ home purchases across Nebraska with over 200 five-star reviews from homeowners who were in situations just like yours. If you want to explore whether a cash sale makes sense before committing to the bankruptcy process, we'd encourage you to get a no-obligation cash offer. It costs nothing and gives you one more option to compare.

Conclusion:

Chapter 7 bankruptcy can be a genuine, powerful lifeline for the right person in the right situation. For Nebraskans with income below the median and primarily unsecured debt, it can eliminate tens of thousands of dollars of financial burden in just a few months. That's real, and it's worth understanding clearly.

But for homeowners, especially those with meaningful equity, the total cost of Chapter 7 bankruptcy isn't only measured in dollars. It's measured in the risk to your home, the decade-long mark on your credit, and the months of legal proceedings required to resolve.

Before you file, make sure you've genuinely compared all of your options. Talk to a licensed Nebraska bankruptcy attorney to understand exactly where you stand on the Means Test and exemption limits. And if you own a home, it’s important to compare all available options before making a final decision. Because for many homeowners, that offer is the fastest, most complete path to financial freedom available.

At Launch Homebuyers, there's no cost and no obligation to find out.

Frequently Asked Questions About Chapter 7 Bankruptcy Cost

How much does Chapter 7 bankruptcy cost in Nebraska?

The total cost to file Chapter 7 bankruptcy in Nebraska typically ranges from $1,900 to $2,400 for a standard consumer case. This includes the $338 federal court filing fee, attorney fees of $1,500–$2,000, two mandatory credit counseling courses ($30–$60), and a recommended credit report ($50).

What is the Chapter 7 court filing fee in Nebraska?

The Chapter 7 court filing fee is $338, set by federal law and uniform across all U.S. bankruptcy courts. It comprises a $245 base fee, a $78 administrative fee, and a $15 trustee surcharge. This amount is paid directly to the court and is required before your case opens.

What happens to my house if I file Chapter 7 bankruptcy in Nebraska?

Your home is protected up to $60,000 in equity under Nebraska's homestead exemption. If your equity stays within this limit and you're current on mortgage payments, you can typically keep your home by signing a reaffirmation agreement. Equity above the exemption threshold may be seized by the bankruptcy trustee.

Is selling my house a way to avoid bankruptcy?

Yes, for many homeowners, a cash home sale generates enough proceeds to pay off all qualifying debts without filing bankruptcy. Unlike Chapter 7, a cash sale carries no credit impact, closes in as few as 7 days, and lets you keep your equity rather than risking it in a trustee review.

How long does Chapter 7 bankruptcy take in Nebraska?

A standard Nebraska Chapter 7 case takes approximately 90 to 120 days from the date of filing to the court's issuance of the final discharge order. Creditor protection through the automatic stay begins the moment your petition is filed, providing immediate relief from collection actions throughout the process.

We are a real estate solutions and investment firm that specializes in helping homeowners get rid of burdensome houses fast. We are investors and problem solvers who can buy your house fast with a fair all cash offer.